When it comes to planning for retirement, a few simple rules can make complex concepts easier to understand. Two of the most helpful are the Rule of 72 and the Rule of 55. Both can give you quick insight into how your savings work and how you can make more informed decisions with your retirement plan.

The Rule of 72: How Fast Will Your Money Double?

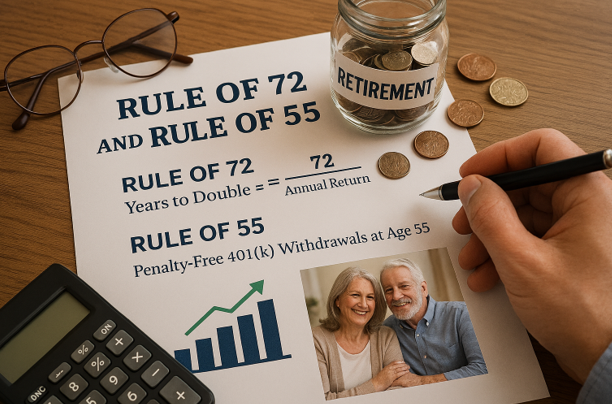

The Rule of 72 is a quick mental shortcut to estimate how long it will take your money to double based on your rate of return. Just divide 72 by your expected rate of return.

Example:

If your retirement account earns a 7% average annual return, your money doubles roughly every 10 years (72 ÷ 7 = ~10.3).

Why it matters for employees:

• It helps you understand the power of starting early.

• It shows how even small increases in contributions or investment return can significantly grow your balance over time.

• It encourages long-term thinking rather than getting discouraged by short-term market noise.

The Rule of 55: Accessing Retirement Savings Penalty-Free

The Rule of 55 is an IRS provision that allows you to take penalty-free withdrawals from your employer-sponsored retirement plan (like a 401(k) or 403(b)) if you leave your job in or after the calendar year you turn 55.

Key points:

• It applies only to the plan sponsored by the employer you just left not to old plans or IRAs.

• Withdrawals are still taxable, but the 10% early withdrawal penalty is waived.

• This rule can be especially helpful for employees considering early retirement, a career change, or a phased transition out of the workforce.

How employees can use this in planning:

• Build flexibility into your retirement strategy knowing this option exists can reduce pressure.

• If you’re planning to retire early, you may leave money in your current employer’s plan to take advantage of the penalty-free access.

• Use it as a bridge until Social Security or other income sources begin.

Why These Rules Matter Together

While the Rule of 72 helps you understand growth, the Rule of 55 helps you understand access. One encourages long-term accumulation; the other provides short-term flexibility. Together, they give employees a clearer picture of both how their retirement savings grow and how they can be used as life plans evolve.

Scott Higgins | AIF ®, CFP®, CPFA®, NSSA®

Financial Advisor

Securities and Investment Advisory Services Offered Through M Holdings Securities, Inc., a Registered Broker/Dealer and Investment Adviser, Member FINRA/SIPC. Rose Street Advisors is independently owned and operated. #5059399